Finance & Economics of Xinjiang ›› 2022, Vol. 0 ›› Issue (3): 50-57.DOI: 10.16716/j.cnki.65-1030/f.2022.03.005

Previous Articles Next Articles

DENG Xiaolan1, LI Yeqin2

Received:

Online:

Published:

邓晓兰1, 李夜衾2

作者简介:

基金资助:

Abstract:

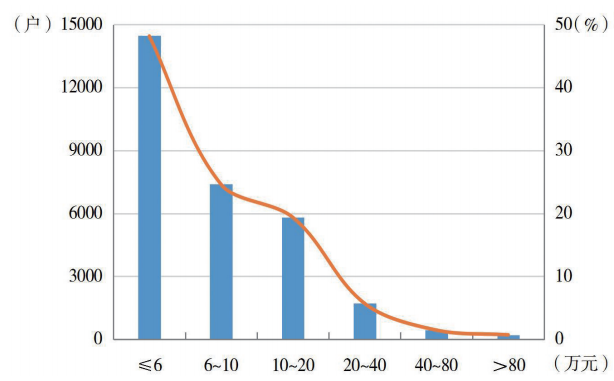

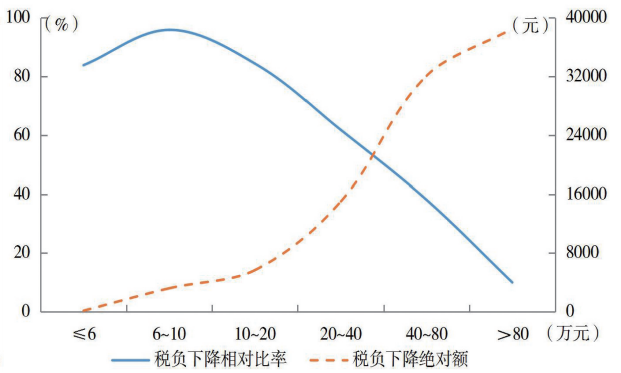

Based on the data of China Household Finance Survey (CHFS) in 2017, this paper uses the micro-simulation method to measure the tax reduction effect of the new individual income tax system from three aspects, overall income, different income groups and different income sources, using the average tax rate and average tax rate. The results show that the individual income tax reform has tax reduction effect on all income groups, but the degree of tax reduction is different for different income groups. The tax reduction amplitude changes with the increase of pre-tax household annual income in an inverted U-shape, that is, with the increase of pre-tax household annual income, the tax burden decreases after the first increase. Tax reform policies, such as raising the basic expense deduction, introducing special additional deductions and adjusting the tax rate structure, have different tax reduction effects among different income groups. Under the comprehensive taxation mode, the tax burden of comprehensive income decreases while that of business income increases. In this regard, it is of necessity to establish a dynamic adjustment mechanism for the deduction of basic expenses so that more low-income groups can enjoy the dividends of special additional deductions. At the same time, efforts should be made to reduce the number of tax rates, reduce the top marginal tax rate and expand the range of low tax rates. For households that have both comprehensive income and operating income, they should be allowed to deduct from their operating income related expenses that are not deducted from their comprehensive income.

Key words: individual income tax, tax reduction effect, personal income tax reform, micro simulation measurement

摘要:

本文基于中国家庭金融调查(CHFS)2017年数据,采用微观模拟法,运用平均税率和平均税额两个指标,从总体、不同收入群体和不同收入来源3个方面,测算了新个人所得税制的减税效应。研究发现:个人所得税改革对所有收入群体都产生了减税效应,但对不同收入群体的减税程度不同,减税幅度随税前家庭年收入的提高呈“倒U形”变化,即随着税前家庭年收入的提高,税负下降相对比率先提高后下降;提高基本费用扣除、引入专项附加扣除和调整税率结构等税改政策在不同收入群体中产生的减税效应不同;综合课税模式下综合所得的税负降低,经营所得的税负升高。对此,应建立基本费用扣除动态调整机制,让更多低收入群体享受到专项附加扣除的红利;同时,需在减少税率级次、降低最高边际税率、扩大低税率级距等方面下工夫;对于同时拥有综合所得和经营所得的家庭,应允许在经营所得中扣除其在综合所得中未扣除的相关费用。

关键词: 个人所得税, 减税效应, 个人所得税改革, 微观模拟测算

CLC Number:

F812.42

DENG Xiaolan, LI Yeqin. Tax Reduction Effect on China's New Personal Income Tax System and Policy Inspirations—Simulation Calculation Based on CHFS Micro-Survey Data[J]. Finance & Economics of Xinjiang, 2022, 0(3): 50-57.

邓晓兰, 李夜衾. 我国新个人所得税制减税效应与政策启示——基于CHFS微观调查数据的模拟测算[J]. 新疆财经, 2022, 0(3): 50-57.

0 / / Recommend

Add to citation manager EndNote|Ris|BibTeX

URL: https://bjb.xjufe.edu.cn/EN/10.16716/j.cnki.65-1030/f.2022.03.005

https://bjb.xjufe.edu.cn/EN/Y2022/V0/I3/50