Finance & Economics of Xinjiang ›› 2023, Issue (5): 16-28.doi: 10.16716/j.cnki.65-1030/f.2023.05.002

Previous Articles Next Articles

GONG Zhenting1,2, CHEN Yanbei1,2

Received:2022-11-03

Online:2023-10-25

Published:2023-09-20

CLC Number:

GONG Zhenting, CHEN Yanbei. The Spillover of Carbon Trading Market, Energy Market and Low Carbon Stock Market—An Empirical Study Based on the Joint Spillover Index Model[J]. Finance & Economics of Xinjiang, 2023, (5): 16-28.

"

| 指标 | 符号 | 来源 |

|---|---|---|

| 中国低碳指数 | LCI | Wind |

| 欧盟碳交易市场每日收盘价格 | EUA | Wind |

| 深圳碳交易市场每日收盘价格 | SZA | Wind |

| 上海碳交易市场每日收盘价格 | SHEA | Wind |

| 广东碳交易市场每日收盘价格 | GDEA | Wind |

| 湖北碳交易市场每日收盘价格 | HBEA | Wind |

| 动力煤价格指数 | COAL | Choice |

| 卓创石油价格指数 | OIL | Choice |

"

| 变量 | 均值 | 中位数 | 标准差 | 偏度 | 峰度 | JB检验 | 观察值 |

|---|---|---|---|---|---|---|---|

| LCI | -0.000525 | -0.000435 | 0.010165 | 0.387307 | 8.443529 | 2128.839 | 1690 |

| EUA | -0.001729 | -0.001441 | 0.021936 | 0.688489 | 11.480250 | 5197.499 | 1690 |

| COAL | 0.000626 | 0.000437 | 0.013578 | -1.561218 | 22.763070 | 28189.790 | 1690 |

| OIL | 0.000215 | 0.000798 | 0.020045 | 0.031162 | 28.197980 | 44710.510 | 1690 |

| SZA | -0.000922 | 0.000000 | 0.328548 | 0.384144 | 22.733410 | 27462.350 | 1690 |

| SHEA | 0.000077 | 0.000000 | 0.027245 | -0.298728 | 20.088610 | 20588.260 | 1690 |

| GDEA | 0.000797 | 0.000264 | 0.022756 | -0.272974 | 10.188700 | 3659.936 | 1690 |

| HBEA | 0.000412 | 0.000000 | 0.022840 | -0.165766 | 9.319908 | 2820.269 | 1690 |

"

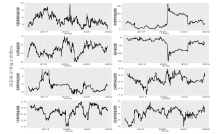

| 指标 | LCI | EUA | COAL | OIL | SZA | SHEA | GDEA | HBEA | |

|---|---|---|---|---|---|---|---|---|---|

| LCI | 99.02 | 0.18 | 0.01 | 0.23 | 0.36 | 0.04 | 0.07 | 0.10 | 1.03 |

| EUA | 0.38 | 98.70 | 0.03 | 0.34 | 0.04 | 0.23 | 0.14 | 0.13 | 1.28 |

| COAL | 0.71 | 0.02 | 98.14 | 0.70 | 0.12 | 0.07 | 0.20 | 0.05 | 1.86 |

| OIL | 1.22 | 6.35 | 0.30 | 90.70 | 0.09 | 0.64 | 0.34 | 0.36 | 9.24 |

| SZA | 0.36 | 0.09 | 0.12 | 0.17 | 98.37 | 0.37 | 0.15 | 0.38 | 1.65 |

| SHEA | 0.43 | 0.13 | 0.05 | 0.80 | 0.38 | 97.44 | 0.69 | 0.08 | 2.55 |

| GDEA | 0.06 | 0.16 | 0.13 | 0.42 | 0.01 | 0.70 | 98.40 | 0.12 | 1.59 |

| HBEA | 0.11 | 0.18 | 0.22 | 0.40 | 0.74 | 0.08 | 0.18 | 98.09 | 1.92 |

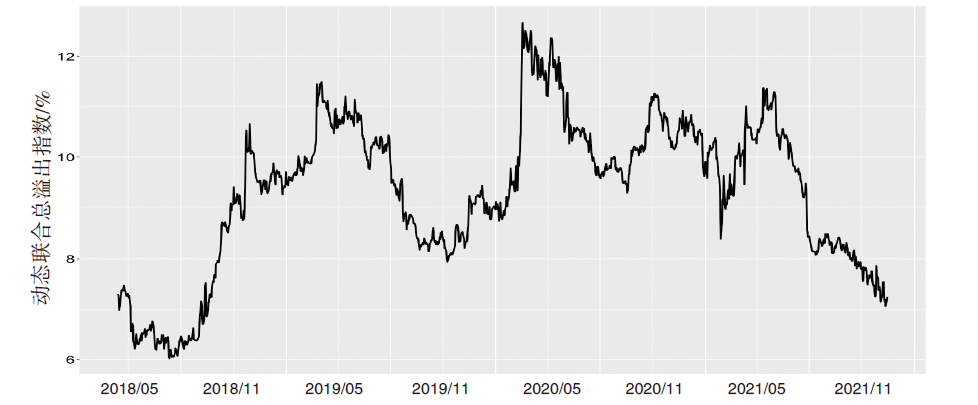

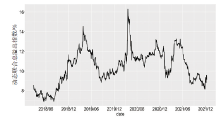

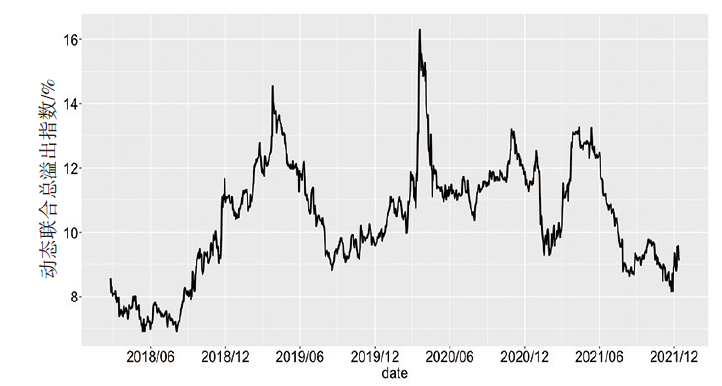

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | jSOI=2.64 | |

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.70 |

"

"

"

"

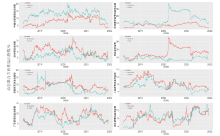

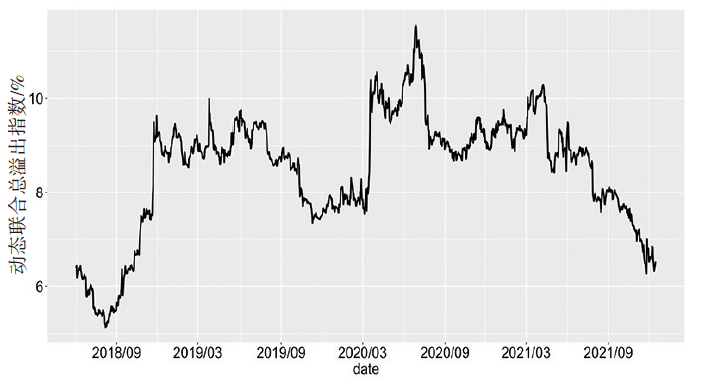

| 预测期 | 变量 | LCI | EUA | COAL | OIL | SZA | SHEA | GDEA | HBEA |

|---|---|---|---|---|---|---|---|---|---|

| H=25 | 1.03 | 1.28 | 1.86 | 9.24 | 1.65 | 2.55 | 1.59 | 1.92 | |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | ||

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.70 | ||

| H=50 | 1.03 | 1.28 | 1.86 | 9.24 | 1.65 | 2.55 | 1.59 | 1.92 | |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | ||

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.7 |

"

"

| [1] | JIANG Y H, LIU L, MU J Q. Nonlinear dependence between China’s carbon market and stock market: new evidence from quantile coherency and causality-in-quantiles[J]. Environmental science and pollution research, 2022(30): 46064-46076. |

| [2] | 张希良, 张达, 余润心. 中国特色全国碳市场设计理论与实践[J]. 管理世界, 2021(8):80-94. |

| [3] |

龚旭, 姬强, 林伯强. 能源金融研究回顾与前沿方向探索[J]. 系统工程理论与实践, 2021(12):3349-3365.

doi: 10.12011/SETP2020-0163 |

| [4] | LIN B Q, CHEN Y F. Dynamic linkages and spillover effects between CET market,coal market and stock market of new energy companies:a case of Beijing CET market in China[J]. Energy, 2019(172):1198-1210. |

| [5] | JI Q, ZHANG D Y, GENG J B. Information linkage,dynamic spillovers in prices and volatility between the carbon and energy markets[J]. Journal of cleaner production, 2018(198):972-978. |

| [6] | 杨冰清, 张侠. 碳交易对中国低碳指数的溢出效应[J]. 山西能源学院学报, 2021(4):39-41. |

| [7] | DIEBOLD F X, YILMAZ K. Measuring financial asset return and volatility spillovers,with application to global equity markets[J]. Economic journal, 2009(534):158-171. |

| [8] | DIEBOLD F X, YILMAZ K. On the network topology of variance decompositions:measuring the connectedness of financial firms[J]. Journal of econometrics, 2014(1):119-134. |

| [9] | 赵领娣, 范超, 王海霞. 中国碳市场与能源市场的时变溢出效应:基于溢出指数模型的实证研究[J]. 北京理工大学学报(社会科学版), 2021(1):28-40. |

| [10] | LASTRAPES W, WIESEN T. The joint spillover index[J]. Economic modelling, 2021(94):681-691. |

| [11] | 魏巍贤, 林伯强. 国内外石油价格波动性及其互动关系[J]. 经济研究, 2007(12):130-141. |

| [12] | 刘明磊, 姬强, 范英. 金融危机前后国内外石油市场风险传导机制研究[J]. 数理统计与管理, 2014(1):9-20. |

| [13] | 张大永, 姬强. 中国原油期货动态风险溢出研究[J]. 中国管理科学, 2018(11):42-49. |

| [14] | GONG X, WEN F H, XIA X H. Investigating the risk-return trade-off for crude oil futures using high-frequency data[J]. Elsevier, 2017(196):152-161. |

| [15] | LIU T Y, GONG X. Analyzing time-varying volatility spillovers between the crude oil markets using a new method[J]. Energy economics, 2020(87):104711. |

| [16] | AN S F, GAO X Y, AN H Z, et al. Windowed volatility spillover effects among crude oil prices[J]. Energy, 2020 (200):117521. |

| [17] | DAI Z F, ZHU H Y. Time-varying spillover effects and investment strategies between WTI crude oil,natural gas and Chinese stock markets related to belt and road initiative[J]. Energy economics, 2022(108):105883. |

| [18] | GONG X, LIU Y, WANG X. Dynamic volatility spillovers across oil and natural gas futures markets based on a time- varying spillover method[J]. International review of financial analysis, 2021(76):101790. |

| [19] | WALID M, UR R M, VINH V X. Dynamic frequency relationships and volatility spillovers in natural gas,crude oil, gas oil,gasoline,and heating oil markets:implications for portfolio management[J]. Resources policy, 2021(73):102172. |

| [20] | ZHONG J, WANG M, DRAKEFORD B M. Spillover effects between oil and natural gas prices:evidence from emerging and developed markets[J]. Green finance, 2019(1):30-45. |

| [21] | KUMAR S, PRADHAN A K, TIWARI A K, et al. Correlations and volatility spillovers between oil,natural gas, and stock prices in India[J]. Resources policy, 2019(62):282-291. |

| [22] | JI Q, GENG J B, TIWARI A K. Information spillovers and connectedness networks in the oil and gas markets[J]. Energy economics, 2018(75):71-84. |

| [23] | REN X H, YUE D, DONG K Y, et al. Information spillover and market connectedness:multi-scale quantile-on- quantile analysis of the crude oil and carbon markets[J]. Applied economics, 2022(38):4465-4485. |

| [24] | DOU Y, LI Y Y, DONG K Y, et al. Dynamic linkages between economic policy uncertainty and the carbon futures market: does Covid-19 pandemic matter?[J]. Resources policy, 2022(75):102455. |

| [25] | CHANG K, YE Z, WANG W. Volatility spillover effect and dynamic correlation between regional emissions allowances and fossil energy markets:new evidence from China’s emissions trading scheme pilots[J]. Energy, 2019(10): 1314-1324. |

| [26] |

刘建和, 梁佳丽, 陈霞. 我国碳市场与国内焦煤市场、欧盟碳市场的溢出效应研究[J]. 工业技术经济, 2020 (9):88-95.

doi: 10.3969/j.issn.1004-910X.2020.09.011 |

| [27] | WANG Y D, GUO Z Y. The dynamic spillover between carbon and energy markets:new evidence[J]. Energy, 2018(149):24-33. |

| [28] | XU Y Y. Risk spillover from energy market uncertainties to the Chinese carbon market[J]. Pacific-basin finance journal, 2021(67):101561. |

| [29] | 曾林, 叶永卫, 王耀德. 碳交易价格对企业创新的影响:基于中国上市公司的实证研究[J]. 上海金融, 2021 (11):61-70. |

| [30] | WEN F, WU N, GONG X. China’s carbon emissions tradingand stock returns[J]. Energy economics, 2020(86): 104627. |

| [31] |

王竹葳, 孙浩瀚, 宋成松. 投资者关注与碳交易市场收益率:基于面板数据的实证研究[J]. 工业技术经济, 2021 (10):3-14.

doi: 10.3969/j.issn.1004-910X.2021.10.001 |

| [32] | 赵选民, 魏雪. 传统能源价格与我国碳交易价格关系研究:基于我国七个碳排放权交易试点省市的面板数据[J]. 生态经济, 2019(2):31-34+52. |

| [33] | NIE D, LI Y B, LI X Y. Dynamic spillovers and asymmetric spillover effect between the carbon emission trading market,fossil energy market,and new energy stock market in China[J]. Energies, 2021(19):6438-6438. |

| [34] | 卜文珂, 赵蒙恩. 碳排放权价格对能源企业股价的影响研究:基于传统能源和新能源企业的对比分析[J]. 价格理论与实践, 2020(3):107-110. |

| [35] | 曾清. 我国碳排放权价格对两类能源公司股价的影响:基于VECM模型的比较分析[J]. 金融发展研究, 2018(10):63-71. |

| [36] | DIEBOLD F X, YILMAZ K. Better to give than to receive:predictive directional measurement of volatility spillovers[J]. International journal of forecasting, 2012(1):57-66. |

| [37] | ANTONAKAKIS N, GABAUER D, GUPTA R, et al. Dynamic connectedness of uncertainty across developed economies: a time-varying approach[J]. Economics letters, 2018(166):63-75. |

| [38] | 龚振庭. 中国碳交易市场与能源市场的时变溢出效应:基于联合溢出指数模型的实证研究[J]. 西部经济管理论坛, 2023(2):49-63. |

| [39] | 陈凡, 龚振庭. 中国股市、欧盟碳市场对中国碳市场价格的影响[J]. 企业经济, 2023(3):48-57. |

| [40] | KUMAR T A, AIKINS A E J, SIMON Y O. Tail risk dependence,co-movement and predictability between green bond and green stocks[J]. Applied economics, 2023(2):201-222. |

| [41] | LIU J T. Time-frequency correlations and extreme spillover effects between carbon markets and NFTs:the roles of EPU and COVID-19[J]. Finance research letters, 2023(54):103690. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||