Finance & Economics of Xinjiang ›› 2025, Vol. 0 ›› Issue (1): 51-57.DOI: 10.16716/j.cnki.65-1030/f.2025.01.005

Previous Articles Next Articles

ZHANG Kaiqiang

Received:

Online:

Published:

张凯强

作者简介:

基金资助:

Abstract:

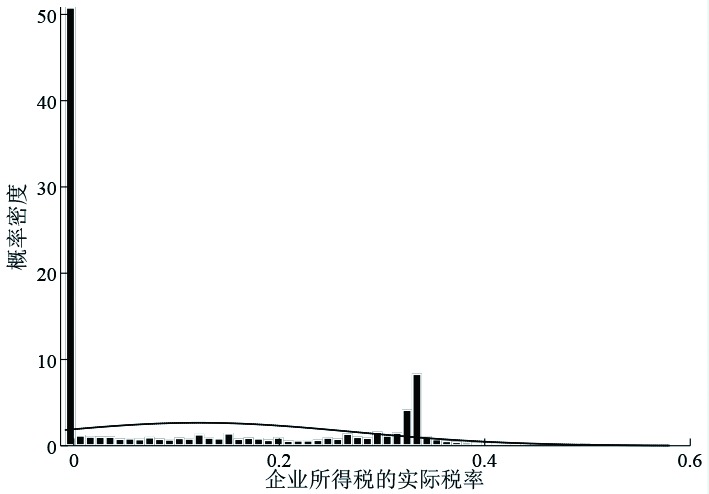

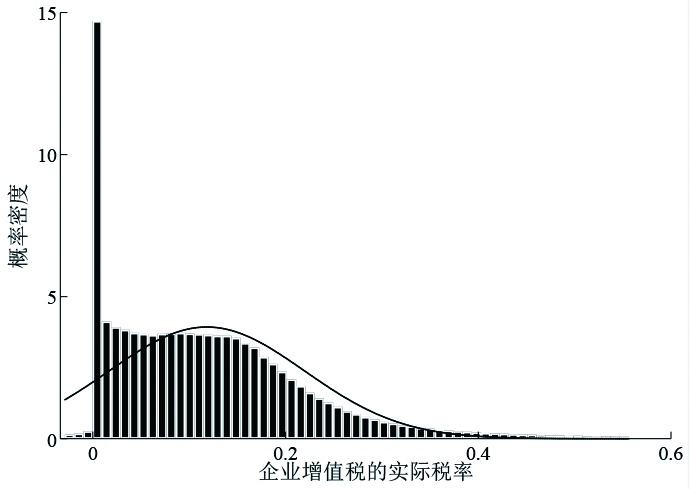

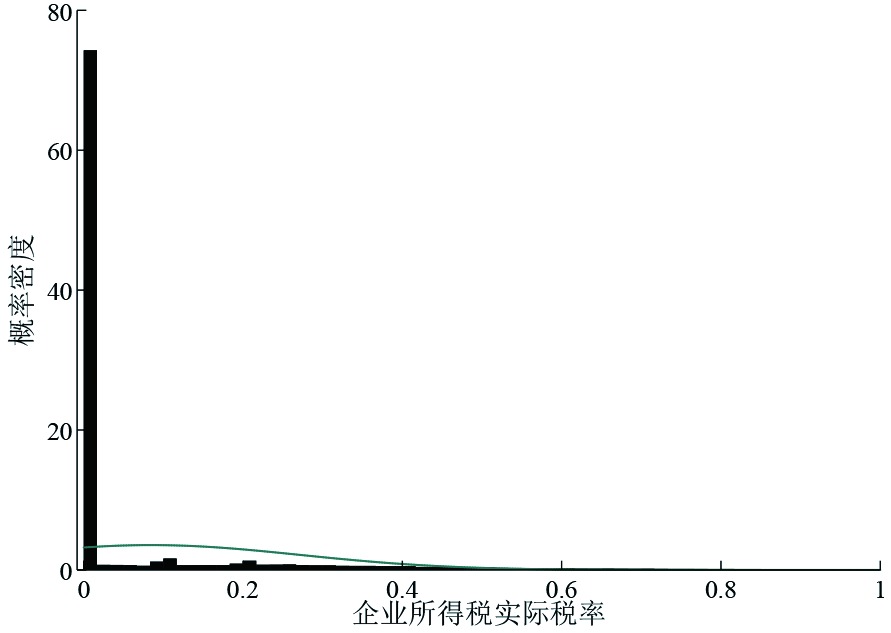

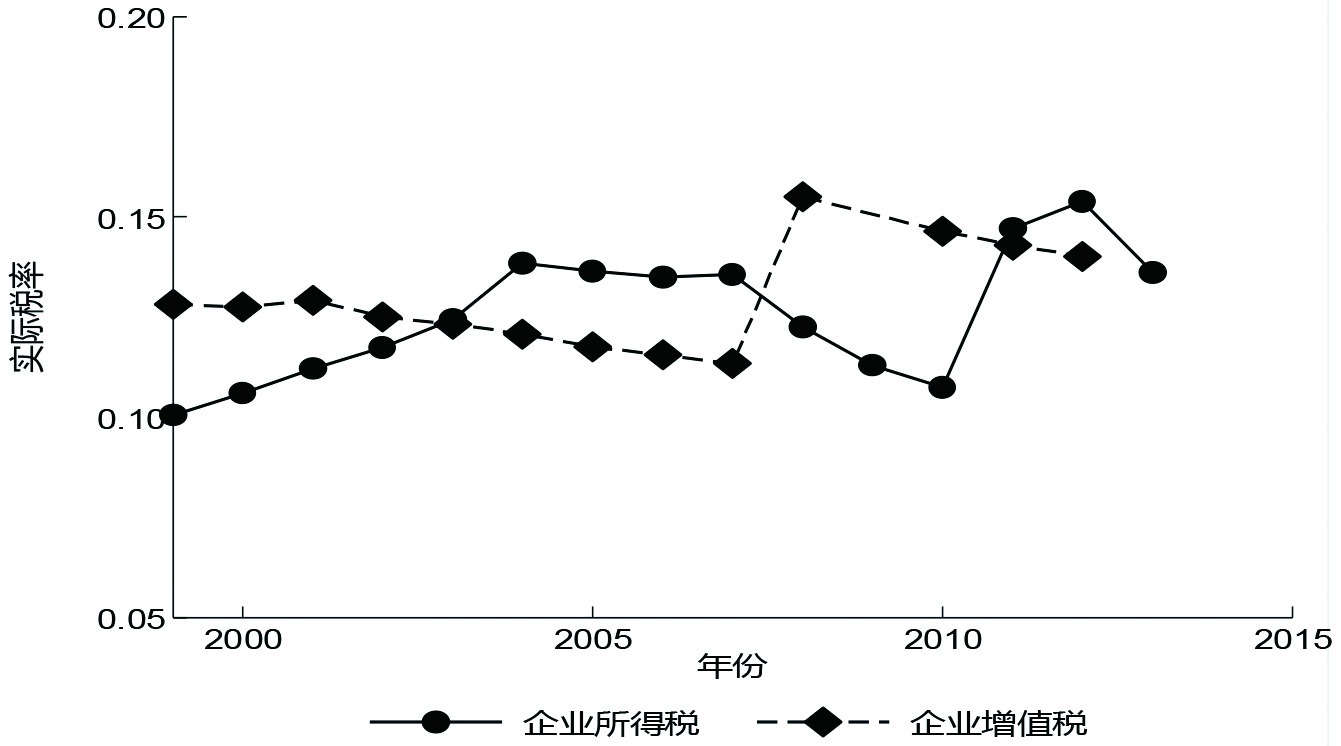

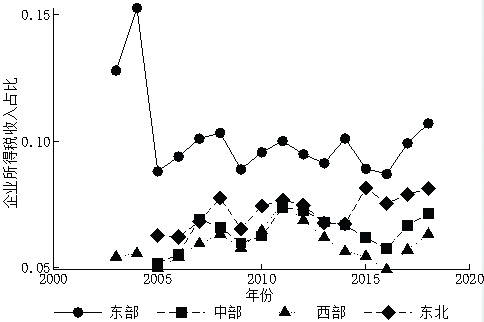

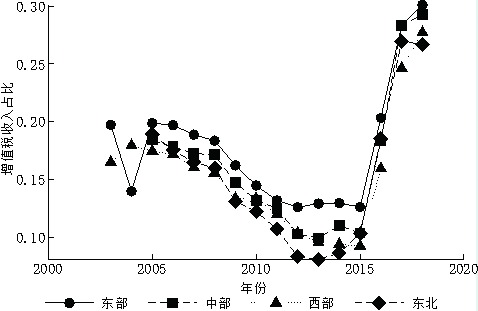

In the new development stage, efforts should be made to build a high-standard market system and consolidate the institutional foundation for the effective operation of the socialist market economy. In this process, reducing the tax burden disparity among enterprises and optimizing the market competition environment are the urgent issues that need to be addressed in China at present. Based on the typical facts of the tax burden disparity among enterprises in China, this paper re-examines the issue of the fairness of the tax burden among enterprises. The research finds that the significant differences in regional tax preferential policies, the varying levels and intensities of tax collection and administration, and the relationship between the government and the market are all reasons for the tax burden disparity among enterprises in China, the tax burden disparity among enterprises is the result of the trade-off between fairness and efficiency. In the future, the tax system structure should be further optimized, the efficiency and consistency of tax policy adjustments should be maintained, the management of enterprise taxes and fees should be standardized, the unification and legalization of tax preferential policies should be achieved, and the tax collection and administration service level of tax authorities should be continuously improved to enhance the coordination of tax collection and administration among regions.

Key words: tax burden, corporate tax burden, high standard market system, fair competition

摘要:

新发展阶段,应努力建设高标准市场体系,筑牢社会主义市场经济有效运行的体制基础。在这一过程中,减少企业间税收负担差异、促进税负公平、优化市场竞争环境等是需重点关注的问题。文章基于我国企业间税收负担差异性的典型事实,重新审视企业间税收负担的公平性问题。研究发现,地区间税收优惠政策差别较大、税收征管水平和强度不同以及政府和市场之间的关系等都是造成我国企业间税收负担差异化的原因,企业税收负担差异化是公平与效率权衡的结果。今后,应进一步优化税制结构,保持税收政策调整的高效性、一致性,规范企业税费管理,实现税收优惠政策的统一化与法治化,不断提高税务机关的征管服务水平,增强地区间税收征管的协调性,更好地促进税负公平。

关键词: 税收负担, 企业税负, 高标准市场体系, 公平竞争

CLC Number:

F812.2

ZHANG Kaiqiang. Re-examination of the Fairness of Corporate Tax Burden from the Perspective of High Standard Market System[J]. Finance & Economics of Xinjiang, 2025, 0(1): 51-57.

张凯强. 高标准市场体系视角下企业税收负担公平性再考察[J]. 新疆财经, 2025, 0(1): 51-57.

0 / / Recommend

Add to citation manager EndNote|Ris|BibTeX

URL: https://bjb.xjufe.edu.cn/EN/10.16716/j.cnki.65-1030/f.2025.01.005

https://bjb.xjufe.edu.cn/EN/Y2025/V0/I1/51