新疆财经 ›› 2023, Vol. 0 ›› Issue (5): 16-28.DOI: 10.16716/j.cnki.65-1030/f.2023.05.002

龚振庭1,2, 陈妍蓓1,2

收稿日期:2022-11-03

出版日期:2023-10-25

发布日期:2023-09-20

作者简介:龚振庭(1993—),男,湛江幼儿师范专科学校经济管理系助教,岭南师范学院基础教育学院助教,研究方向为金融风险管理、绿色金融;基金资助:GONG Zhenting1,2, CHEN Yanbei1,2

Received:2022-11-03

Online:2023-10-25

Published:2023-09-20

摘要:

随着全国统一的碳交易市场建设步伐的逐步加快,科学衡量不同市场之间的风险溢出效应对于有效应对复杂多变的市场情况尤为重要。文章运用联合溢出指数模型,实证发现碳交易市场、能源市场与低碳股票市场之间存在风险溢出效应,且不同市场间的方向性溢出效应和净溢出效应存在明显的时变特征;相较于我国,欧盟碳交易市场的抗风险能力更强。对此,应建立碳交易市场、能源市场与低碳股票市场之间的风险预警机制,完善我国碳交易市场的政策体系和相关金融机构的信息披露机制,从而有效防范跨市场间的金融风险。

中图分类号:

龚振庭, 陈妍蓓. 碳交易市场、能源市场与低碳股票市场的风险溢出效应——基于联合溢出指数模型的实证研究[J]. 新疆财经, 2023, 0(5): 16-28.

GONG Zhenting, CHEN Yanbei. The Spillover of Carbon Trading Market, Energy Market and Low Carbon Stock Market—An Empirical Study Based on the Joint Spillover Index Model[J]. Finance & Economics of Xinjiang, 2023, 0(5): 16-28.

| 指标 | 符号 | 来源 |

|---|---|---|

| 中国低碳指数 | LCI | Wind |

| 欧盟碳交易市场每日收盘价格 | EUA | Wind |

| 深圳碳交易市场每日收盘价格 | SZA | Wind |

| 上海碳交易市场每日收盘价格 | SHEA | Wind |

| 广东碳交易市场每日收盘价格 | GDEA | Wind |

| 湖北碳交易市场每日收盘价格 | HBEA | Wind |

| 动力煤价格指数 | COAL | Choice |

| 卓创石油价格指数 | OIL | Choice |

表1 指标定义与数据来源

| 指标 | 符号 | 来源 |

|---|---|---|

| 中国低碳指数 | LCI | Wind |

| 欧盟碳交易市场每日收盘价格 | EUA | Wind |

| 深圳碳交易市场每日收盘价格 | SZA | Wind |

| 上海碳交易市场每日收盘价格 | SHEA | Wind |

| 广东碳交易市场每日收盘价格 | GDEA | Wind |

| 湖北碳交易市场每日收盘价格 | HBEA | Wind |

| 动力煤价格指数 | COAL | Choice |

| 卓创石油价格指数 | OIL | Choice |

| 变量 | 均值 | 中位数 | 标准差 | 偏度 | 峰度 | JB检验 | 观察值 |

|---|---|---|---|---|---|---|---|

| LCI | -0.000525 | -0.000435 | 0.010165 | 0.387307 | 8.443529 | 2128.839 | 1690 |

| EUA | -0.001729 | -0.001441 | 0.021936 | 0.688489 | 11.480250 | 5197.499 | 1690 |

| COAL | 0.000626 | 0.000437 | 0.013578 | -1.561218 | 22.763070 | 28189.790 | 1690 |

| OIL | 0.000215 | 0.000798 | 0.020045 | 0.031162 | 28.197980 | 44710.510 | 1690 |

| SZA | -0.000922 | 0.000000 | 0.328548 | 0.384144 | 22.733410 | 27462.350 | 1690 |

| SHEA | 0.000077 | 0.000000 | 0.027245 | -0.298728 | 20.088610 | 20588.260 | 1690 |

| GDEA | 0.000797 | 0.000264 | 0.022756 | -0.272974 | 10.188700 | 3659.936 | 1690 |

| HBEA | 0.000412 | 0.000000 | 0.022840 | -0.165766 | 9.319908 | 2820.269 | 1690 |

表2 指标的描述性统计结果

| 变量 | 均值 | 中位数 | 标准差 | 偏度 | 峰度 | JB检验 | 观察值 |

|---|---|---|---|---|---|---|---|

| LCI | -0.000525 | -0.000435 | 0.010165 | 0.387307 | 8.443529 | 2128.839 | 1690 |

| EUA | -0.001729 | -0.001441 | 0.021936 | 0.688489 | 11.480250 | 5197.499 | 1690 |

| COAL | 0.000626 | 0.000437 | 0.013578 | -1.561218 | 22.763070 | 28189.790 | 1690 |

| OIL | 0.000215 | 0.000798 | 0.020045 | 0.031162 | 28.197980 | 44710.510 | 1690 |

| SZA | -0.000922 | 0.000000 | 0.328548 | 0.384144 | 22.733410 | 27462.350 | 1690 |

| SHEA | 0.000077 | 0.000000 | 0.027245 | -0.298728 | 20.088610 | 20588.260 | 1690 |

| GDEA | 0.000797 | 0.000264 | 0.022756 | -0.272974 | 10.188700 | 3659.936 | 1690 |

| HBEA | 0.000412 | 0.000000 | 0.022840 | -0.165766 | 9.319908 | 2820.269 | 1690 |

| 指标 | LCI | EUA | COAL | OIL | SZA | SHEA | GDEA | HBEA | |

|---|---|---|---|---|---|---|---|---|---|

| LCI | 99.02 | 0.18 | 0.01 | 0.23 | 0.36 | 0.04 | 0.07 | 0.10 | 1.03 |

| EUA | 0.38 | 98.70 | 0.03 | 0.34 | 0.04 | 0.23 | 0.14 | 0.13 | 1.28 |

| COAL | 0.71 | 0.02 | 98.14 | 0.70 | 0.12 | 0.07 | 0.20 | 0.05 | 1.86 |

| OIL | 1.22 | 6.35 | 0.30 | 90.70 | 0.09 | 0.64 | 0.34 | 0.36 | 9.24 |

| SZA | 0.36 | 0.09 | 0.12 | 0.17 | 98.37 | 0.37 | 0.15 | 0.38 | 1.65 |

| SHEA | 0.43 | 0.13 | 0.05 | 0.80 | 0.38 | 97.44 | 0.69 | 0.08 | 2.55 |

| GDEA | 0.06 | 0.16 | 0.13 | 0.42 | 0.01 | 0.70 | 98.40 | 0.12 | 1.59 |

| HBEA | 0.11 | 0.18 | 0.22 | 0.40 | 0.74 | 0.08 | 0.18 | 98.09 | 1.92 |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | jSOI=2.64 | |

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.70 |

表3 静态溢出指数/%

| 指标 | LCI | EUA | COAL | OIL | SZA | SHEA | GDEA | HBEA | |

|---|---|---|---|---|---|---|---|---|---|

| LCI | 99.02 | 0.18 | 0.01 | 0.23 | 0.36 | 0.04 | 0.07 | 0.10 | 1.03 |

| EUA | 0.38 | 98.70 | 0.03 | 0.34 | 0.04 | 0.23 | 0.14 | 0.13 | 1.28 |

| COAL | 0.71 | 0.02 | 98.14 | 0.70 | 0.12 | 0.07 | 0.20 | 0.05 | 1.86 |

| OIL | 1.22 | 6.35 | 0.30 | 90.70 | 0.09 | 0.64 | 0.34 | 0.36 | 9.24 |

| SZA | 0.36 | 0.09 | 0.12 | 0.17 | 98.37 | 0.37 | 0.15 | 0.38 | 1.65 |

| SHEA | 0.43 | 0.13 | 0.05 | 0.80 | 0.38 | 97.44 | 0.69 | 0.08 | 2.55 |

| GDEA | 0.06 | 0.16 | 0.13 | 0.42 | 0.01 | 0.70 | 98.40 | 0.12 | 1.59 |

| HBEA | 0.11 | 0.18 | 0.22 | 0.40 | 0.74 | 0.08 | 0.18 | 98.09 | 1.92 |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | jSOI=2.64 | |

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.70 |

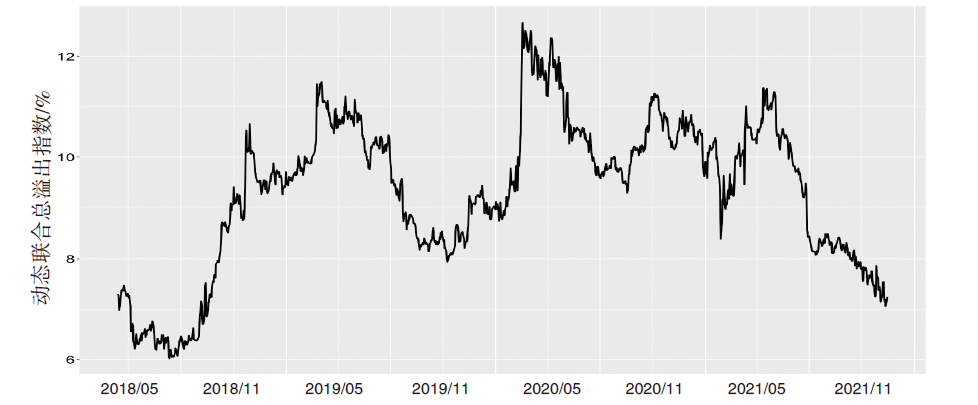

图1 动态联合总溢出指数

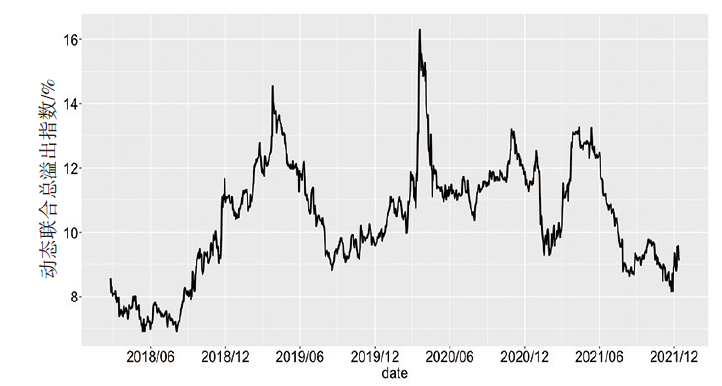

图2 动态联合方向性溢出指数

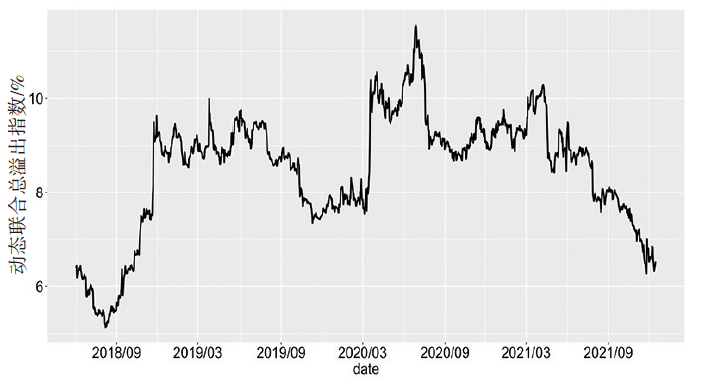

图3 动态联合净溢出指数

| 预测期 | 变量 | LCI | EUA | COAL | OIL | SZA | SHEA | GDEA | HBEA |

|---|---|---|---|---|---|---|---|---|---|

| H=25 | 1.03 | 1.28 | 1.86 | 9.24 | 1.65 | 2.55 | 1.59 | 1.92 | |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | ||

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.70 | ||

| H=50 | 1.03 | 1.28 | 1.86 | 9.24 | 1.65 | 2.55 | 1.59 | 1.92 | |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | ||

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.7 |

表4 不同预测期数的静态溢出指数/%

| 预测期 | 变量 | LCI | EUA | COAL | OIL | SZA | SHEA | GDEA | HBEA |

|---|---|---|---|---|---|---|---|---|---|

| H=25 | 1.03 | 1.28 | 1.86 | 9.24 | 1.65 | 2.55 | 1.59 | 1.92 | |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | ||

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.70 | ||

| H=50 | 1.03 | 1.28 | 1.86 | 9.24 | 1.65 | 2.55 | 1.59 | 1.92 | |

| 3.27 | 7.11 | 0.86 | 3.06 | 1.73 | 2.13 | 1.77 | 1.22 | ||

| 2.23 | 5.83 | -1.00 | -6.19 | 0.08 | -0.42 | 0.18 | -0.7 |

图4 滚动窗口为300期的动态联合总溢出指数

图5 滚动窗口为400期的动态联合总溢出指数

| [1] | JIANG Y H, LIU L, MU J Q. Nonlinear dependence between China’s carbon market and stock market: new evidence from quantile coherency and causality-in-quantiles[J]. Environmental science and pollution research, 2022(30): 46064-46076. |

| [2] | 张希良, 张达, 余润心. 中国特色全国碳市场设计理论与实践[J]. 管理世界, 2021(8):80-94. |

| [3] |

龚旭, 姬强, 林伯强. 能源金融研究回顾与前沿方向探索[J]. 系统工程理论与实践, 2021(12):3349-3365.

DOI |

| [4] | LIN B Q, CHEN Y F. Dynamic linkages and spillover effects between CET market,coal market and stock market of new energy companies:a case of Beijing CET market in China[J]. Energy, 2019(172):1198-1210. |

| [5] | JI Q, ZHANG D Y, GENG J B. Information linkage,dynamic spillovers in prices and volatility between the carbon and energy markets[J]. Journal of cleaner production, 2018(198):972-978. |

| [6] | 杨冰清, 张侠. 碳交易对中国低碳指数的溢出效应[J]. 山西能源学院学报, 2021(4):39-41. |

| [7] | DIEBOLD F X, YILMAZ K. Measuring financial asset return and volatility spillovers,with application to global equity markets[J]. Economic journal, 2009(534):158-171. |

| [8] | DIEBOLD F X, YILMAZ K. On the network topology of variance decompositions:measuring the connectedness of financial firms[J]. Journal of econometrics, 2014(1):119-134. |

| [9] | 赵领娣, 范超, 王海霞. 中国碳市场与能源市场的时变溢出效应:基于溢出指数模型的实证研究[J]. 北京理工大学学报(社会科学版), 2021(1):28-40. |

| [10] | LASTRAPES W, WIESEN T. The joint spillover index[J]. Economic modelling, 2021(94):681-691. |

| [11] | 魏巍贤, 林伯强. 国内外石油价格波动性及其互动关系[J]. 经济研究, 2007(12):130-141. |

| [12] | 刘明磊, 姬强, 范英. 金融危机前后国内外石油市场风险传导机制研究[J]. 数理统计与管理, 2014(1):9-20. |

| [13] | 张大永, 姬强. 中国原油期货动态风险溢出研究[J]. 中国管理科学, 2018(11):42-49. |

| [14] | GONG X, WEN F H, XIA X H. Investigating the risk-return trade-off for crude oil futures using high-frequency data[J]. Elsevier, 2017(196):152-161. |

| [15] | LIU T Y, GONG X. Analyzing time-varying volatility spillovers between the crude oil markets using a new method[J]. Energy economics, 2020(87):104711. |

| [16] | AN S F, GAO X Y, AN H Z, et al. Windowed volatility spillover effects among crude oil prices[J]. Energy, 2020 (200):117521. |

| [17] | DAI Z F, ZHU H Y. Time-varying spillover effects and investment strategies between WTI crude oil,natural gas and Chinese stock markets related to belt and road initiative[J]. Energy economics, 2022(108):105883. |

| [18] | GONG X, LIU Y, WANG X. Dynamic volatility spillovers across oil and natural gas futures markets based on a time- varying spillover method[J]. International review of financial analysis, 2021(76):101790. |

| [19] | WALID M, UR R M, VINH V X. Dynamic frequency relationships and volatility spillovers in natural gas,crude oil, gas oil,gasoline,and heating oil markets:implications for portfolio management[J]. Resources policy, 2021(73):102172. |

| [20] | ZHONG J, WANG M, DRAKEFORD B M. Spillover effects between oil and natural gas prices:evidence from emerging and developed markets[J]. Green finance, 2019(1):30-45. |

| [21] | KUMAR S, PRADHAN A K, TIWARI A K, et al. Correlations and volatility spillovers between oil,natural gas, and stock prices in India[J]. Resources policy, 2019(62):282-291. |

| [22] | JI Q, GENG J B, TIWARI A K. Information spillovers and connectedness networks in the oil and gas markets[J]. Energy economics, 2018(75):71-84. |

| [23] | REN X H, YUE D, DONG K Y, et al. Information spillover and market connectedness:multi-scale quantile-on- quantile analysis of the crude oil and carbon markets[J]. Applied economics, 2022(38):4465-4485. |

| [24] | DOU Y, LI Y Y, DONG K Y, et al. Dynamic linkages between economic policy uncertainty and the carbon futures market: does Covid-19 pandemic matter?[J]. Resources policy, 2022(75):102455. |

| [25] | CHANG K, YE Z, WANG W. Volatility spillover effect and dynamic correlation between regional emissions allowances and fossil energy markets:new evidence from China’s emissions trading scheme pilots[J]. Energy, 2019(10): 1314-1324. |

| [26] |

刘建和, 梁佳丽, 陈霞. 我国碳市场与国内焦煤市场、欧盟碳市场的溢出效应研究[J]. 工业技术经济, 2020 (9):88-95.

DOI |

| [27] | WANG Y D, GUO Z Y. The dynamic spillover between carbon and energy markets:new evidence[J]. Energy, 2018(149):24-33. |

| [28] | XU Y Y. Risk spillover from energy market uncertainties to the Chinese carbon market[J]. Pacific-basin finance journal, 2021(67):101561. |

| [29] | 曾林, 叶永卫, 王耀德. 碳交易价格对企业创新的影响:基于中国上市公司的实证研究[J]. 上海金融, 2021 (11):61-70. |

| [30] | WEN F, WU N, GONG X. China’s carbon emissions tradingand stock returns[J]. Energy economics, 2020(86): 104627. |

| [31] |

王竹葳, 孙浩瀚, 宋成松. 投资者关注与碳交易市场收益率:基于面板数据的实证研究[J]. 工业技术经济, 2021 (10):3-14.

DOI |

| [32] | 赵选民, 魏雪. 传统能源价格与我国碳交易价格关系研究:基于我国七个碳排放权交易试点省市的面板数据[J]. 生态经济, 2019(2):31-34+52. |

| [33] | NIE D, LI Y B, LI X Y. Dynamic spillovers and asymmetric spillover effect between the carbon emission trading market,fossil energy market,and new energy stock market in China[J]. Energies, 2021(19):6438-6438. |

| [34] | 卜文珂, 赵蒙恩. 碳排放权价格对能源企业股价的影响研究:基于传统能源和新能源企业的对比分析[J]. 价格理论与实践, 2020(3):107-110. |

| [35] | 曾清. 我国碳排放权价格对两类能源公司股价的影响:基于VECM模型的比较分析[J]. 金融发展研究, 2018(10):63-71. |

| [36] | DIEBOLD F X, YILMAZ K. Better to give than to receive:predictive directional measurement of volatility spillovers[J]. International journal of forecasting, 2012(1):57-66. |

| [37] | ANTONAKAKIS N, GABAUER D, GUPTA R, et al. Dynamic connectedness of uncertainty across developed economies: a time-varying approach[J]. Economics letters, 2018(166):63-75. |

| [38] | 龚振庭. 中国碳交易市场与能源市场的时变溢出效应:基于联合溢出指数模型的实证研究[J]. 西部经济管理论坛, 2023(2):49-63. |

| [39] | 陈凡, 龚振庭. 中国股市、欧盟碳市场对中国碳市场价格的影响[J]. 企业经济, 2023(3):48-57. |

| [40] | KUMAR T A, AIKINS A E J, SIMON Y O. Tail risk dependence,co-movement and predictability between green bond and green stocks[J]. Applied economics, 2023(2):201-222. |

| [41] | LIU J T. Time-frequency correlations and extreme spillover effects between carbon markets and NFTs:the roles of EPU and COVID-19[J]. Finance research letters, 2023(54):103690. |

| [1] | 李季鹏, 石甲香. 耐心资本对企业韧性的影响研究[J]. 新疆财经, 2025, 0(4): 59-69. |

| [2] | 潘超, 张波. 商业银行数字化转型、收入多元化转型与经营稳定性[J]. 新疆财经, 2025, 0(4): 37-46. |

| [3] | 施志晖, 杜苏迪, 陆岷峰. 扎根理论视角下数字人民币生态圈利益相关者互动机制研究[J]. 新疆财经, 2025, 0(1): 40-50. |

| [4] | 郭洋, 胡茂林, 龚刚强. “双碳”背景下绿色金融与绿色科技区域协同耦合研究[J]. 新疆财经, 2024, 0(6): 29-39. |

| [5] | 邱静, 张锦. 文过饰非:股权质押与MD&A文本信息粉饰——基于机器学习文本分析方法的实证研究[J]. 新疆财经, 2024, 0(4): 37-47. |

| [6] | 祝志川, 蒋犇. 基于动态CRITIC赋权的中国金融压力指数构建与金融风险识别[J]. 新疆财经, 2024, 0(1): 21-33. |

| [7] | 刘剑锋. 国际原油市场与中国股票市场的波动溢出效应——基于滚窗VAR模型的测度[J]. 新疆财经, 2023, 0(4): 15-24. |

| [8] | 雷汉云, 李棋, 玉素甫·阿布来提. 金融科技促进经济高质量发展的理论逻辑与实践路径[J]. 新疆财经, 2023, 0(4): 37-47. |

| [9] | 宋清华, 谭晓熳. 绿色信贷能推动产业结构绿色转型升级吗?——基于我国省级面板数据的实证研究[J]. 新疆财经, 2023, 0(3): 29-35. |

| [10] | 朱晓燕, 黄政, 邱静暄. 年报柔性监管与股价崩盘风险——基于年报问询函语调的研究[J]. 新疆财经, 2023, 0(3): 47-56. |

| [11] | 王淑杰, 曹晓倩. 政府引导基金对产业结构升级的影响效应研究[J]. 新疆财经, 2023, 0(2): 39-47. |

| [12] | 高晓燕, 翟振山, 付赛飞. 金融集聚对绿色经济绩效的影响研究[J]. 新疆财经, 2023, 0(1): 38-46. |

| [13] | 谢婷婷, 高丽丽, 冯梅菊. 政府干预、银行业竞争与民营企业融资约束[J]. 新疆财经, 2022, 0(6): 33-44. |

| [14] | 宁泽逵, 王哲, 屈桥. 中国互联网金融风险研究进展与展望[J]. 新疆财经, 2022, 0(6): 23-32. |

| [15] | 于博, 林龙斌. 退市制度改革降低摘帽企业二次戴帽风险了吗?[J]. 新疆财经, 2022, 0(5): 24-37. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||